Michigan Cannabis Market Q2 2026: Prices, Licenses, and What Operators Need to Know

Michigan’s cannabis market just posted its strongest single sales day in history. On 4/20, the state moved $20.4 million in one day (Hemp Gazette, May 2026). April adult-use sales hit $258.17 million, bouncing back hard from a January low of $224.4 million. By pure sales volume, Michigan is the #2 cannabis market in the country, trailing only California’s $311.2 million in April.

So everything’s great, right? Not if you’re growing it.

The Michigan cannabis industry in 2026 is a paradox. Consumers are buying more cannabis than ever. Retailers are moving record volume. And the cultivators supplying all of it are getting squeezed harder every quarter. If you’re operating a commercial cannabis grow in Michigan right now, this is the field guide for Q2. Not predictions. Not investor-grade optimism. Just the numbers, the regulatory shifts, and what the operators who are still standing are actually doing.

The Sales Paradox: More Pounds, Less Money

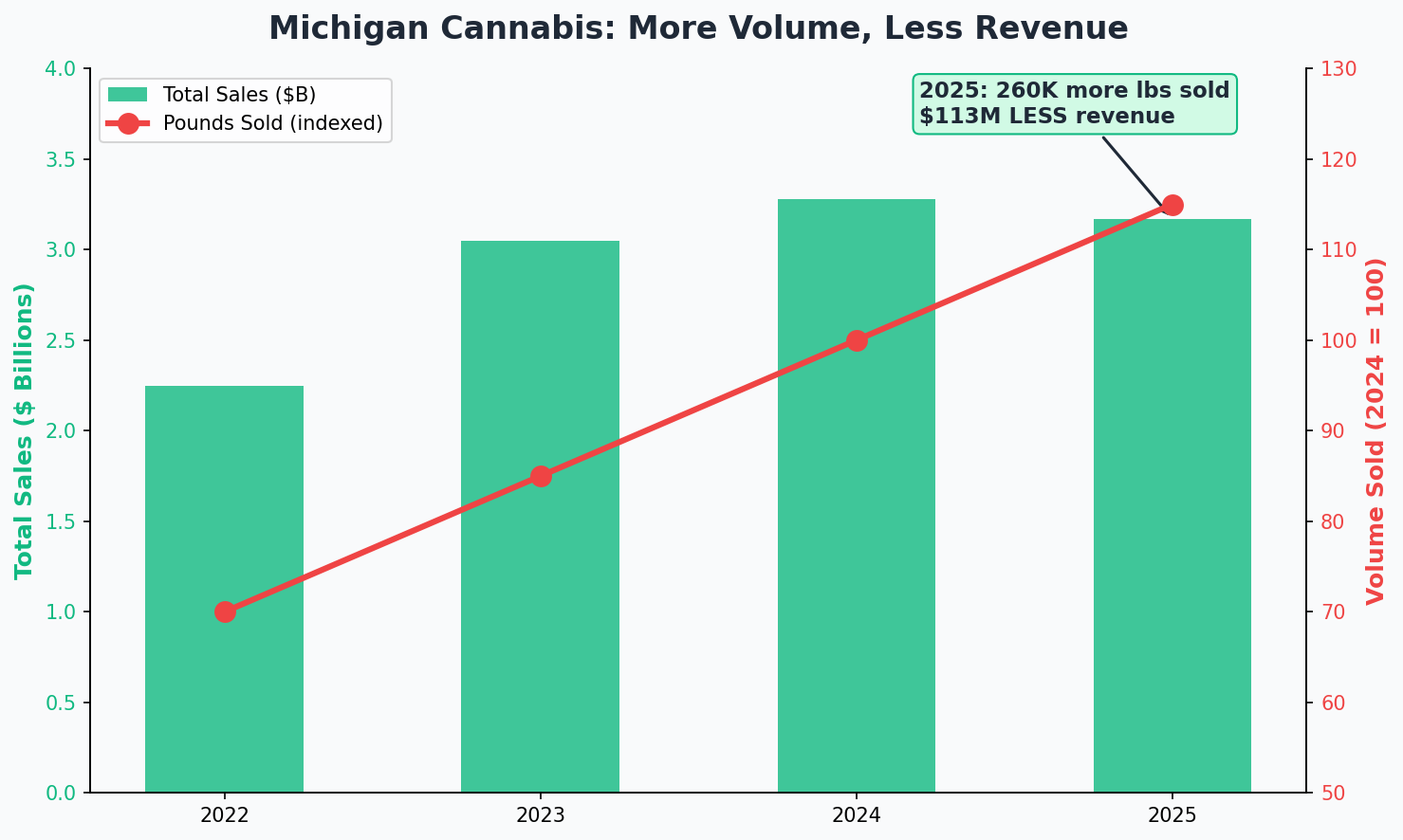

Here’s the number that should be pinned to every cultivation office wall in the state: Michigan sold 260,000 more pounds of cannabis in 2025 than in 2024. Total adult-use revenue for 2025 was $3.17 billion (Michigan CRA data). That sounds like growth until you realize the 2024 total was $3.28 billion. The market moved a quarter million more pounds and generated $113 million less revenue.

Michigan sold 260K more pounds in 2025 than 2024, but generated $113M less revenue. Volume up, revenue down.

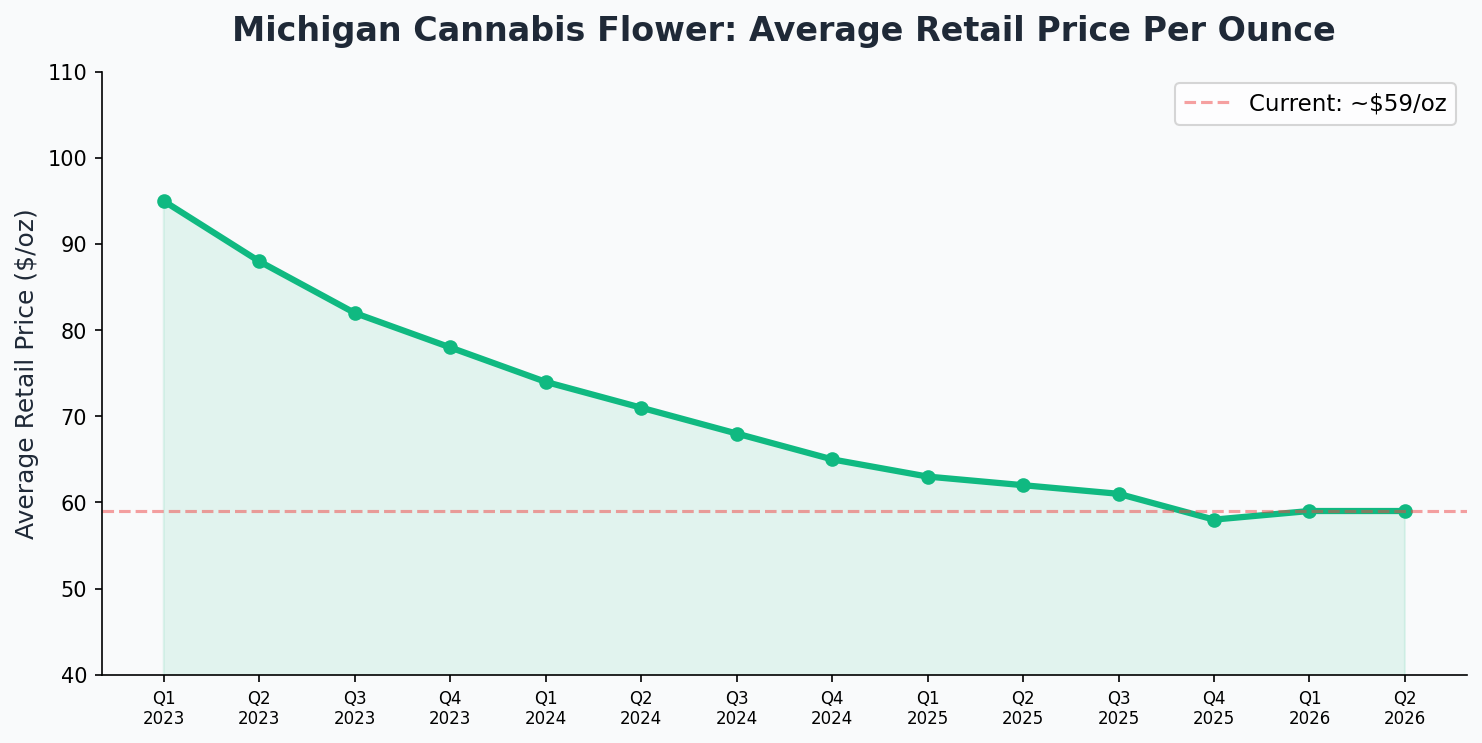

That’s the oversupply cycle in a single data point. Operators produce more to maintain revenue. Prices drop. Margins collapse. So they produce more. Michigan has earned the nickname “the Walmart of weed” for a reason (Crain’s Detroit Business, May 2026). Average retail flower price hit roughly $59 to $62 per ounce in April 2026 according to Weedmaps and CRA data. That’s down from $240+ per ounce just a few years ago. An 8.2% year-over-year decline in February alone (Weedmaps, 2026).

If retail is sitting around $60 an ounce, work backward. Dispensary margins, taxes, testing, transport. The wholesale number that lands in a grower’s pocket is getting brutal. Estimated wholesale flower prices in Michigan are running in the $500 to $600 per pound range for most operators. At that price point, your cost per pound determines whether you’re building a business or subsidizing one. If you’re not tracking what your cost per pound actually is, now is the time: here’s how to calculate the real number.

Wholesale Price Compression Is Still Accelerating

Michigan wholesale cannabis flower prices have been in freefall. The compression is structural, not cyclical.

This price compression isn’t a dip. It’s structural. Michigan has more licensed canopy per capita than almost any state in the country, and the excess capacity hasn’t worked its way out yet. Every quarter, a few more growers close. But the remaining operators are getting more efficient, which means the floor keeps dropping.

The growers who treat this like a temporary slump are the ones closing. The ones treating it as the new normal are investing in consistency, yield optimization, and operational systems that compound over time. If you’re running the same playbook you ran in 2023, the math doesn’t work anymore. The operators pulling ahead are the ones who’ve figured out how to scale output from their existing footprint instead of chasing more canopy.

License Attrition: 940+ Grower Licenses Gone in Six Years

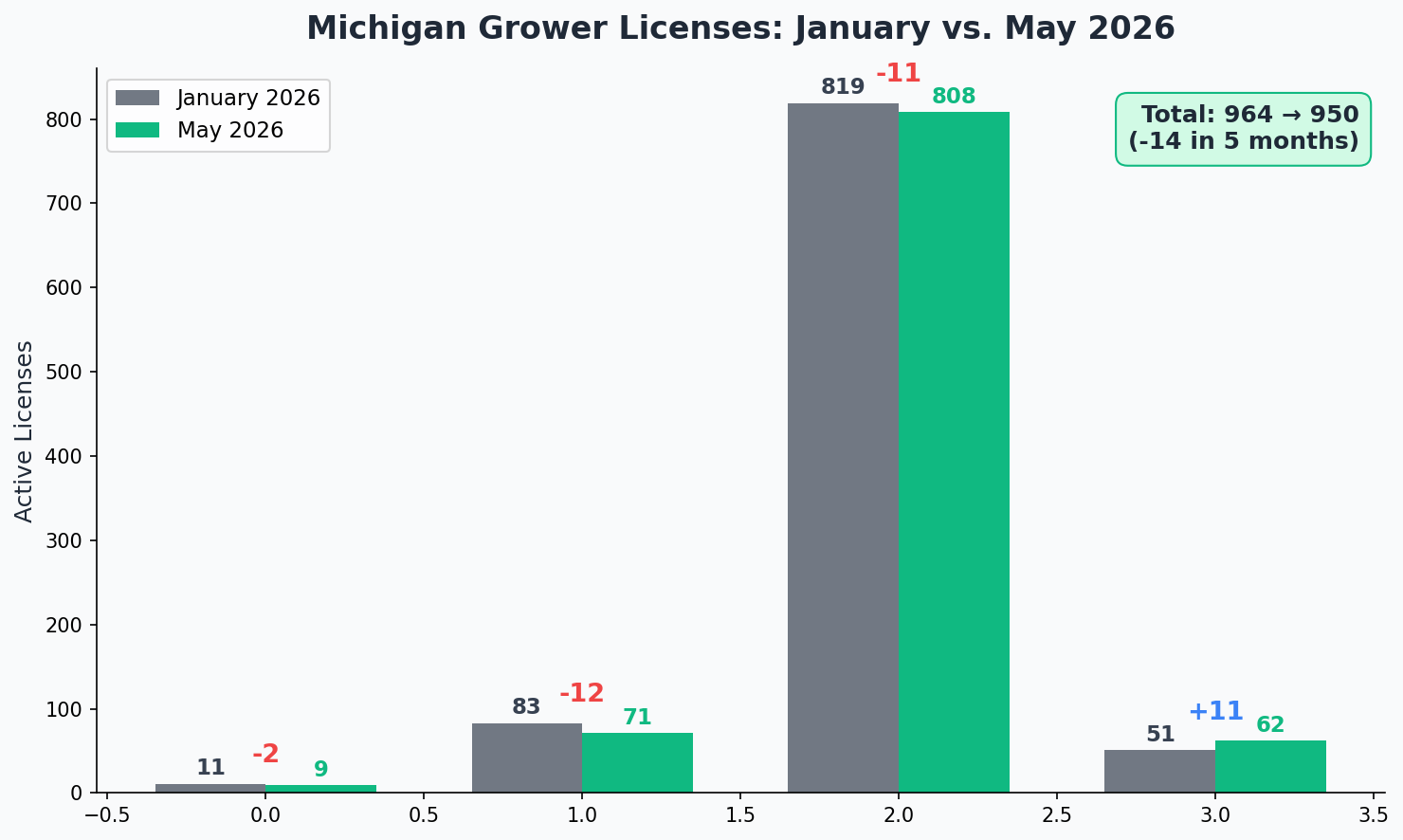

The Michigan CRA database tells the consolidation story clearly. As of May 2026, the state has 950 active grower licenses: 9 Class A, 71 Class B, 808 Class C, and 62 Excess. Back in January 2026, that number was 964. That’s 14 grower licenses gone in five months.

Michigan has shed over 940 grower licenses in six years. 2025 saw the first year-over-year decline: 85 licenses gone.

Zoom out further: over six years, Michigan has lost approximately 940 grower licenses. In 2025 alone, 85 licenses disappeared, marking the first clear year-over-year decline in active grower counts. Nationally, 13% of all cannabis licenses have vanished in the past two years (Headset, 2026). Michigan is contributing heavily to that number.

The smaller operations are under the most pressure. Declining margins, rising compliance costs, insurance, labor. These fixed costs don’t scale down when wholesale prices drop by half. The operators folding aren’t necessarily bad growers. They’re operations where the economics simply stopped working at current price levels. Industry consolidation in Michigan is “likely inevitable” according to market analysts (Crain’s Detroit Business, May 2026).

The 24% Wholesale Tax: A Slow Fuse

Michigan’s new 24% wholesale tax (passed in 2025 legislation) is now in effect. If you haven’t felt it yet, you will. According to Robin Schneider of the Michigan Cannabis Industry Association, retailers are still selling through pre-tax inventory. The full consumer price impact hasn’t hit yet. When it does, the question is simple: does the retailer pass it through to the consumer, or does it get pushed back upstream to the grower?

If you’ve been in this industry for more than a cycle, you already know the answer. In a market with $60 ounces and a customer base trained on bargain pricing, retailers will protect their price point. That tax is going to show up as tighter margins for cultivators, not higher shelf prices. Another reason your cost per pound needs to be as low as you can possibly get it.

Regulatory Shifts: Schedule III, Rec Hearings, and CRA Enforcement

Two big regulatory developments are in play right now.

Medical cannabis moved to Schedule III on April 28, 2026. The immediate impact for operators: Section 280E tax relief. Cannabis businesses can now take standard business deductions that were previously disallowed. This is real money back in your pocket. If your accountant hasn’t updated your quarterly estimates, get on the phone.

Recreational rescheduling hearings begin June 29, 2026. If recreational cannabis also moves to Schedule III, the tax implications expand further. Worth watching, but don’t plan around it yet.

On the enforcement side, the CRA cracked down on 39 cannabis companies in May 2026 for sales, tracking, and security violations (MI Tech News, May 2026). The message is clear: the state is tightening compliance, not loosening it. Running a clean operation isn’t optional. It’s table stakes.

The Ohio Factor

Michigan’s border communities (Monroe, Niles, Benton Harbor) have always drawn out-of-state traffic. With Ohio’s recent THC crackdown pushing enforcement on their side of the border, expect even more buyers to make the drive. This props up retail volume but does almost nothing for wholesale prices. More transactions at $60 an ounce still translates to compressed margins for cultivators.

For operators near the border, it’s worth paying attention to foot traffic patterns. For everyone else, Ohio’s regulatory moves are background noise. Your margins are determined by what happens inside your facility, not what happens at the state line.

What the Surviving Operators Are Doing Differently

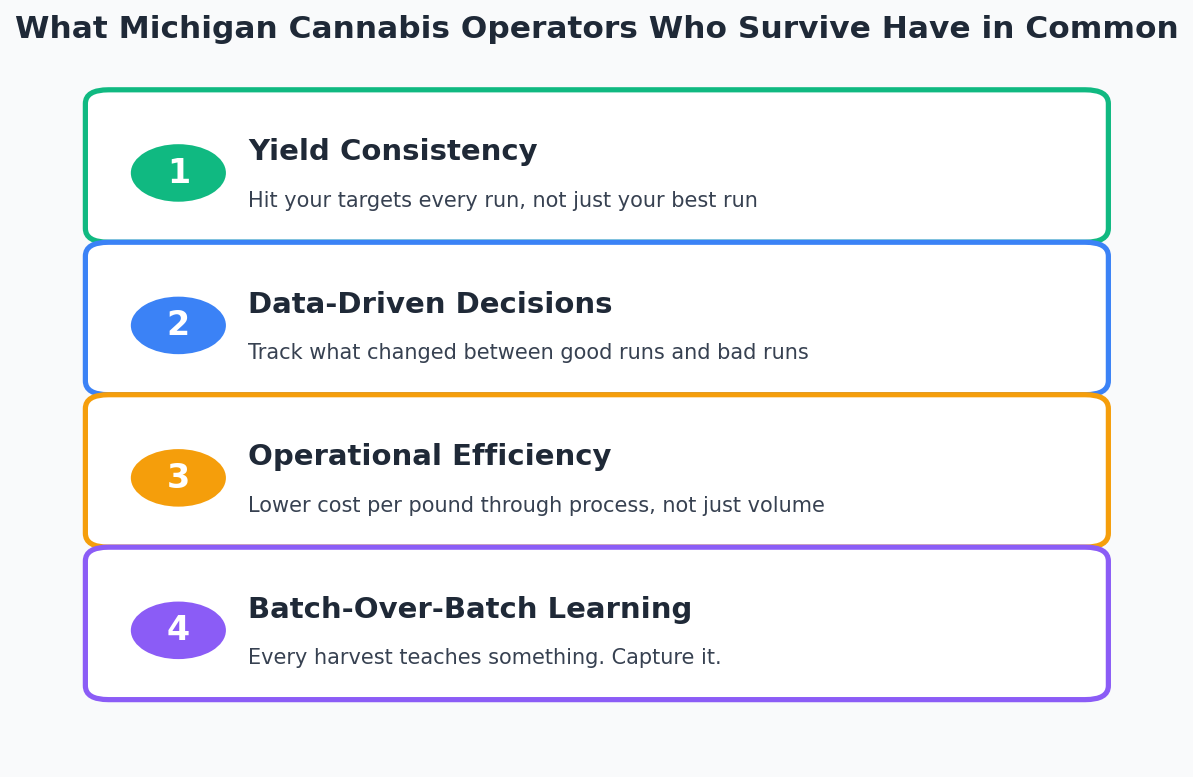

Here’s where it stops being a market report and starts being useful. The Michigan cannabis growers who are surviving (and in some cases growing) in this environment share a few common traits. None of them are secrets. All of them require discipline.

The four factors separating operators who are growing from operators who are closing.

1. They know their cost per pound, and they attack it. Not as a vague concept. As an actual number they can recite. The two primary levers are yield and consistency. Yield is the biggest single driver of low cost per pound. Consistency is the multiplier. Hitting 2.5 lbs per light once is a good story. Hitting it eight runs in a row is a business. If your yields swing 20% between runs, you’re leaving money on the floor every cycle.

2. They track batches and learn from them. Every run is a data set. The operators pulling ahead are the ones who do a real post-harvest review: what worked, what changed, what to carry forward into the next run. The ones who just reset and plant again are repeating the same patterns. In a market this tight, repeating patterns you haven’t examined is expensive.

3. They’ve stopped guessing at environment. VPD drift, DLI inconsistency, overnight temperature swings. These are the invisible yield killers that don’t show up until harvest day. The best operators are connecting environment data to yield outcomes, not just watching a dashboard in real time. Real-time dashboards tell you what’s happening now. Connecting that data to harvest results tells you what actually mattered.

4. They’re building systems, not depending on memory. The “master grower carries everything in their head” model doesn’t scale, and it definitely doesn’t survive a compressed market. When one person holds all the institutional knowledge and that person has a bad week, the whole operation drifts. The surviving facilities are the ones that have systematized their cultivation knowledge so it compounds run over run, regardless of who’s on the floor.

The Real Question for Michigan Cannabis Growers in 2026

This market is not going to get easier. Wholesale prices aren’t recovering to 2021 levels. The 24% tax will compress margins further. More licenses will go dark. That’s not doom. That’s just the maturation curve every agricultural commodity goes through.

The question isn’t whether you have problems. Every operation does. The question is whether your rate of improvement is faster than the rate the market is squeezing you. The growers who survive aren’t the ones with zero issues. They’re the ones who systematize learning so they improve faster than the market compresses.

If you’re still standing in Michigan in May 2026, you’ve already proven you can grow. The next phase is proving you can improve, consistently, run after run, with data backing every decision. That’s the only path forward in a $500 to $600 wholesale market.

Growgoyle doesn’t track your costs. It helps you lower them. In a market this compressed, the only lever you fully control is your cost per pound, and the only way to attack it is better yields and tighter consistency. See the full system built by a grower operating in this exact market. See how it works.

Get Michigan market updates every Wednesday.

The Michigan Cannabis Market Intel newsletter covers wholesale prices, license changes, enforcement actions, and what it all means for operators. Free, no fluff. Sign up here →

Make Every Batch Better Than the Last

METRC tracks your grow for the state. Growgoyle tracks it for you. Batch tracking, live environmental monitoring, AI-powered plant analysis, and side-by-side batch comparison, all in one place.

30-day free trial. No credit card required.

About the Author

Eric is a 15-year software engineer who operates a commercial cannabis cultivation facility in Michigan. He built Growgoyle to solve the problems he faces every day: inconsistent yields, forgotten lessons from past runs, and the constant pressure to lower cost per pound. Every feature in Growgoyle comes from real growing experience, not a product roadmap.

Leave a Reply